Advertisements for e-bike insurance, battery protection plans, extended warranties, and service contracts have become increasingly common.

Many riders see words like “insurance,” “coverage,” “protection,” or “warranty” and assume they understand what is being offered.

The reality is that these products can be very different from one another.

Before spending money on any protection product, take the time to understand exactly what is being sold, who is providing it, how claims are handled, and what documentation supports the coverage.

This article is intended for educational and informational purposes only. It is not intended to recommend or discourage any specific insurance provider, protection plan, warranty, service contract, or business. Consumers should conduct their own research and review the documentation governing any product before making a purchasing decision.

Quick Summary

- Determine what risk you are trying to cover.

- Do not assume every protection product is insurance.

- Verify who provides the coverage.

- Verify important claims using the actual policy, contract, or coverage documents.

- Review coverage documents before purchasing.

- Understand who handles claims and repairs.

- Verify any manufacturer relationship.

- Check existing coverage before purchasing additional products.

- Research public records when appropriate.

- Keep ownership and policy documentation.

- Verify first and purchase second.

What Problem Are You Trying to Solve?

Before purchasing any insurance or protection product, identify the specific risk you are trying to cover.

Common concerns include:

- Theft

- Crash damage

- Battery replacement costs

- Water damage

- Fire damage

- Liability exposure

- Out-of-warranty repairs

Understanding the problem first makes it easier to determine whether a particular product actually addresses that risk.

Not Every Protection Product Is Insurance

One of the most common mistakes consumers make is assuming that every protection product works the same way.

Terms commonly used in advertising include:

- Insurance

- Battery insurance

- Protection plans

- Extended warranties

- Service contracts

- Repair agreements

- Membership programs

These products may operate differently and may provide different types of coverage.

Before purchasing anything, determine exactly what type of product is being offered.

Understand Who Is Providing the Coverage

Before purchasing any protection product, identify the entity responsible for the coverage.

Important questions include:

- Who provides the coverage?

- What legal entity is responsible for claims?

- Is there a licensed insurance carrier involved?

- Is there an underwriter?

- Is the product a service contract rather than insurance?

- What company is responsible for repairs?

You should be able to identify who stands behind the product before making a purchase.

What Is an Underwriter?

In traditional insurance, the underwriter is the company that assumes the financial risk and backs the policy.

Understanding who underwrites a product can help consumers better understand who is ultimately responsible for the coverage being offered.

Not every protection product will involve an insurance underwriter, which is why understanding the type of product being sold is important.

Check Existing Coverage First

Before purchasing a new insurance or protection product, determine whether you already have coverage available through existing policies or programs.

Examples may include:

- Homeowners insurance

- Renters insurance

- Scheduled personal property coverage

- Umbrella policies

- Credit card purchase protections

- Manufacturer warranties

In some cases, consumers may already have protection available and may not need additional coverage.

Questions to Ask Before Buying

Before purchasing any e-bike insurance policy, battery protection plan, service contract, or warranty, consider asking:

- Who provides the coverage?

- Is this insurance, a warranty, or a service contract?

- Who underwrites the coverage?

- Who approves claims?

- Who performs repairs?

- What exclusions apply?

- What are the coverage limits?

- What states is the product available in?

- What documentation can I review before purchasing?

- What is the claims process?

If you cannot clearly understand how the product works, continue researching before spending money.

Think Through Real-World Scenarios

Before purchasing any protection product, think about the events you actually want covered.

Examples include:

- Your battery catches fire.

- A thermal runaway event occurs.

- Your battery is stolen.

- Your bike is stolen.

- Your battery is damaged by water.

- Your charger damages the battery.

- Your bike is involved in a crash.

- The battery damages other property.

- The battery fails after the manufacturer warranty expires.

- A major component fails unexpectedly.

For each scenario, ask:

- Is it covered?

- Is it excluded?

- Is there a deductible?

- Is there a coverage limit?

- What documentation is required?

- Who determines whether the claim is approved?

Do not assume coverage exists simply because a product is advertised.

Verify it before purchasing.

Does the Bike Manufacturer Support the Product?

Before purchasing coverage, determine whether there is any relationship between the provider and the manufacturer of your bike.

Questions worth asking include:

- Is the provider officially recognized by the manufacturer?

- Is there a formal partnership?

- Is the provider an authorized repair facility?

- Are genuine replacement parts used?

- Will using the service affect warranty coverage?

- Does the manufacturer acknowledge the relationship?

The absence of a manufacturer relationship does not automatically indicate a problem, but consumers should understand whether such a relationship exists before purchasing coverage.

The existence or absence of a manufacturer relationship does not by itself determine the quality, value, or legitimacy of a product.

Questions to Ask About Battery Coverage

Battery-related protection plans deserve additional scrutiny because battery replacement can be expensive.

Questions worth asking include:

- Is accidental damage covered?

- Is water damage covered?

- Is theft covered?

- Is capacity degradation covered?

- Is normal wear covered?

- Is fire damage covered?

- Is property damage covered?

- Who determines whether the battery is repairable?

- Who performs repairs or replacements?

- Are there limits on claim frequency?

- Are there coverage caps or deductibles?

Knowing these answers in advance may help avoid surprises later.

If Your Bike Has Modifications

Many riders upgrade their bikes with:

- Batteries

- Controllers

- Motors

- Suspension

- Wheels

- Brakes

- Lighting

- Security systems

Before purchasing coverage, determine whether modifications affect eligibility, claims, repair coverage, or replacement coverage.

A protection plan that only covers stock equipment may not meet the needs of a heavily modified bike.

Understand Exclusions and Waiting Periods

Many consumers focus on what is covered but overlook what is excluded.

Questions worth asking include:

- Is there a waiting period before coverage begins?

- Are pre-existing issues excluded?

- Are modified bikes covered?

- Are aftermarket batteries covered?

- Is commercial use excluded?

- Is racing or competition use excluded?

- Is water damage excluded?

Understanding exclusions may be just as important as understanding coverage.

Marketing Materials Are Not the Contract

Advertisements, social media posts, referral pages, promotional videos, ambassador content, and product summaries can be useful introductions to a product.

Marketing materials are often designed to summarize products and highlight key features.

As a result, they may not contain every coverage limitation, exclusion, condition, deductible, waiting period, or claim requirement that appears in the governing documentation.

Before purchasing, consumers should review the documentation that actually governs the product and verify any features that are important to their decision.

Consumers should review the documents that govern the product rather than relying solely on summaries or promotional descriptions.

Understand Promotional Relationships

People discussing a product online may have different relationships with the provider.

Examples include:

- Customers

- Affiliates

- Ambassadors

- Sponsors

- Influencers

- Referral partners

- Company representatives

These relationships do not automatically make information accurate or inaccurate, but consumers should understand the source of the information they are relying upon.

Consumers should evaluate the information being provided rather than making assumptions based solely on who is providing it.

Promotional content can introduce a product, but it should not replace independent research.

Understanding How Information Changes

When researching any insurance product, protection plan, warranty, or service contract, consumers should understand that information may pass through multiple sources before reaching them.

Examples may include:

- Advertisements

- Social media posts

- Videos

- Referral programs

- Affiliate websites

- Ambassador content

- Online discussions

- Product summaries

As information is repeated, summarized, or interpreted, important details can sometimes be omitted, misunderstood, or communicated inaccurately.

This does not necessarily mean anyone has acted improperly. It simply means consumers should verify important information using the documentation that governs the product.

If a specific feature is important to your purchasing decision, review the relevant documentation and confirm that the feature is actually covered under the terms of the agreement.

The closer you get to the original policy, contract, coverage agreement, or governing documentation, the more reliable your understanding of the product is likely to be.

Coverage, exclusions, limitations, and claim requirements are generally governed by the applicable policy, contract, agreement, or documentation rather than by summaries or promotional descriptions.

Verify Important Claims Before Purchasing

If a specific benefit is important to your purchasing decision, verify it before spending money.

Examples include:

- Battery fire coverage

- Thermal runaway coverage

- Water damage coverage

- Theft coverage

- Crash damage coverage

- Third-party battery coverage

- Modified-bike coverage

- Property damage coverage

Rather than assuming coverage exists, review the governing documentation and ask questions before purchasing.

If a specific claim, feature, or benefit is important to your decision, verify it directly in the governing documentation whenever possible.

The documents governing the product are often more authoritative than summaries, advertisements, referral pages, social media posts, or other promotional content.

Review the Documentation

Before purchasing any protection product, review the available documentation.

Examples may include:

- Policy documents

- Terms and conditions

- Coverage agreements

- Service contract agreements

- Claim procedures

- Exclusion lists

Take the time to read the documents rather than relying solely on advertising materials.

Coverage details often matter far more than marketing language.

When questions arise, the governing documentation is generally a more reliable source of information than advertisements, summaries, or promotional materials.

Get Important Answers in Writing

If a coverage detail is important to you, ask the question in writing and keep the response.

Examples include:

- Is water damage covered?

- Are modifications covered?

- Is theft covered?

- Are aftermarket batteries covered?

- What documentation is required for a claim?

Keeping written responses may help avoid misunderstandings later.

What Will You Need If You File a Claim?

Many claims processes require documentation.

Examples may include:

- Proof of purchase

- Bills of sale

- Serial numbers

- Battery serial numbers

- Photographs

- Police reports

- Repair estimates

- Ownership records

The easier it is to document ownership and the condition of your bike, the easier it may be to support a future claim.

Keep Copies of Everything

Save copies of:

- Policies

- Contracts

- Terms and conditions

- Coverage agreements

- Emails

- Quotes

- Claim submissions

- Claim responses

- Written answers to questions

Documentation can become important if questions arise later.

What Happens If the Provider Stops Operating?

Before purchasing any protection product, consider what happens if the provider changes ownership, closes, declares bankruptcy, or stops offering the program.

Questions worth asking include:

- Who remains responsible for claims?

- Are claims transferred to another company?

- Does coverage survive a business closure?

- Is there a separate insurance carrier involved?

Understanding this before a problem occurs may help avoid surprises later.

Why Licensing and Regulation Exist

Licensing, registration, reporting, and oversight requirements exist in many industries to promote accountability, disclosure, recordkeeping, and consumer protection.

Depending on the product, provider, and jurisdiction involved, consumers may have access to public databases, complaint processes, regulatory resources, and other tools designed to help them research businesses and products.

These resources can help consumers make more informed decisions, but they should be viewed as part of a broader research process rather than a substitute for independent review.

Laws, regulations, licensing requirements, and consumer protections may vary by jurisdiction.

Regulation Does Not Replace Due Diligence

Licensing, registration, and oversight can provide useful information, but consumers should still:

- Review documentation

- Understand exclusions

- Verify coverage details

- Ask questions

- Understand claim procedures

Consumers should view regulation as one source of information rather than the only source of information.

Verify Information Independently

Whenever possible, verify information using independent sources.

Useful resources may include:

- State insurance regulators

- Business registration databases

- Secretary of State business records

- Public court records

- Regulatory databases

- Manufacturer websites

- Official product documentation

Useful resources:

New Jersey Department of Banking and Insurance License Search

https://www-dobi.nj.gov/DOBI_LicSearch/

National Association of Insurance Commissioners State Based Systems License Lookup

https://sbs.naic.org/solar-external-lookup/lookup

Federal Court Records

Research Public Records Carefully

Public records can be useful when researching a business, but they should not be viewed as the only source of information.

Consumers may review:

- Business registrations

- Regulatory records

- Public court filings

- Bankruptcy filings

- Civil litigation records

The existence of a lawsuit, complaint, or regulatory matter does not automatically indicate wrongdoing, and the absence of such records does not automatically validate a business.

Public records often reflect allegations, claims, filings, or proceedings that may or may not be resolved in favor of any particular party.

Public records are only one part of a broader research process.

Advertising Is Not Verification

Advertising can be useful for learning that a product exists, but it should not replace independent research.

Before purchasing any insurance product, protection plan, warranty, or service contract:

- Review the documentation.

- Verify important details.

- Ask questions.

- Confirm who provides the product.

- Understand how claims are handled.

The goal is to make an informed decision based on facts rather than assumptions.

Examples of Protection Products

Consumers may encounter several different types of products in the marketplace.

Insurance Policies

May provide coverage for theft, accidental damage, liability, or other specified events.

Service Contracts

May cover certain repairs or replacement services under specific conditions.

Extended Warranties

May extend certain manufacturer warranty protections beyond the original coverage period.

Battery Protection Plans

May provide repair or replacement benefits depending on the contract terms.

The important point is understanding which product you are purchasing and what obligations the provider has under that agreement.

Situations That May Warrant Additional Research

Additional research may be worthwhile when:

- Coverage details are difficult to obtain.

- Claims procedures are unclear.

- Coverage exclusions are not disclosed.

- Important questions cannot be answered.

- Documentation is unavailable before purchase.

- It is difficult to determine who provides the coverage.

These situations do not automatically indicate a problem, but they may justify further investigation before making a decision.

Keep Good Ownership Records

Regardless of which protection product you choose, maintaining ownership records is important.

Keep:

- Purchase invoices

- Bills of sale

- Serial numbers

- Battery serial numbers

- Photographs

- Upgrade receipts

- Payment records

Many claim processes require supporting documentation.

The easier it is to document ownership and the condition of your bike, the easier it may be to support a future claim.

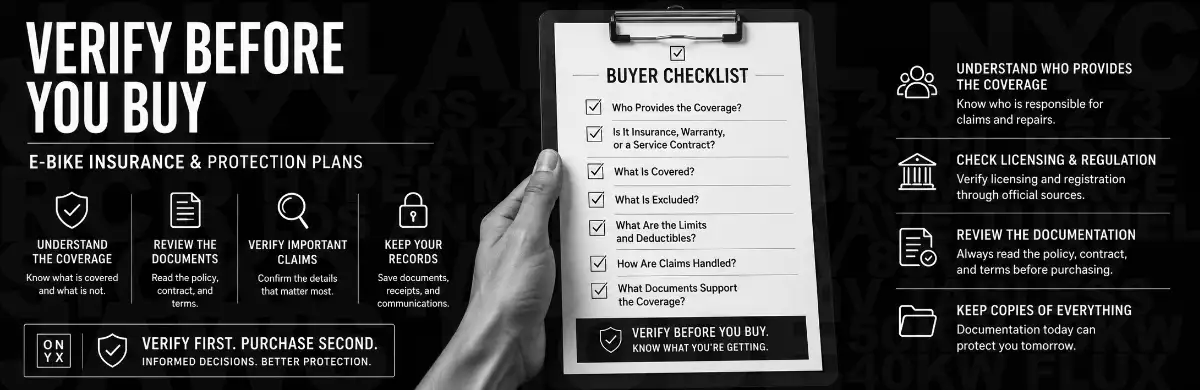

Buyer Verification Checklist

Before purchasing any e-bike insurance policy, battery protection plan, warranty, or service contract:

- Identify the risk you want covered.

- Verify who provides the product.

- Determine whether it is insurance, a warranty, or a service contract.

- Review policy and coverage documents.

- Review exclusions and waiting periods.

- Understand the claims process.

- Determine who performs repairs.

- Verify any manufacturer relationship.

- Check existing coverage.

- Research public records if appropriate.

- Keep ownership documentation.

- Get important answers in writing.

- Verify independently before purchasing.

The Goal Is Understanding

The purpose of due diligence is not to prove that a company is good or bad.

The purpose is to understand:

- What you are buying

- Who provides it

- What documents govern it

- How claims are handled

- What limitations exist

before spending your money.

Final Advice

Insurance policies, warranties, service contracts, and protection plans can all provide value when properly understood.

The mistake many consumers make is purchasing a product based solely on advertising without fully understanding what is being offered.

No advertisement, website, influencer, forum post, or sales pitch should replace your own research.

Before purchasing any e-bike insurance policy, battery protection plan, warranty, or service contract, verify who provides the product, understand what type of product it is, review the documentation, and understand how claims are handled.

The goal is not to determine whether a company, advertisement, influencer, affiliate, ambassador, or referral source is trustworthy. The goal is to understand the product itself.

The closer you get to the actual policy, contract, coverage agreement, or governing documentation, the more reliable your understanding of the product is likely to be.

The purpose of due diligence is not to determine whether a company is good or bad. The purpose is to understand what you are buying before you spend your money.

Verify first. Purchase second.